Signals to pay attention to in African fintech for the rest of 2024

How fintechs are navigating capital, regulation, and market shifts in 2024

Last year, we took a deep dive into African fintech in 2022, analyzing the key developments, recurring themes, and emerging trends that we anticipated would play a key role in the new year. This time, as we move further along into 2024, our focus shifts to the future as we embark on what’s shaping up to be an equally compelling year for fintech on the continent. In true Decode Fintech style, we’ll be exploring what’s working, what’s not, and where fintech in Africa is going next.

How fintechs are navigating the capital crunch

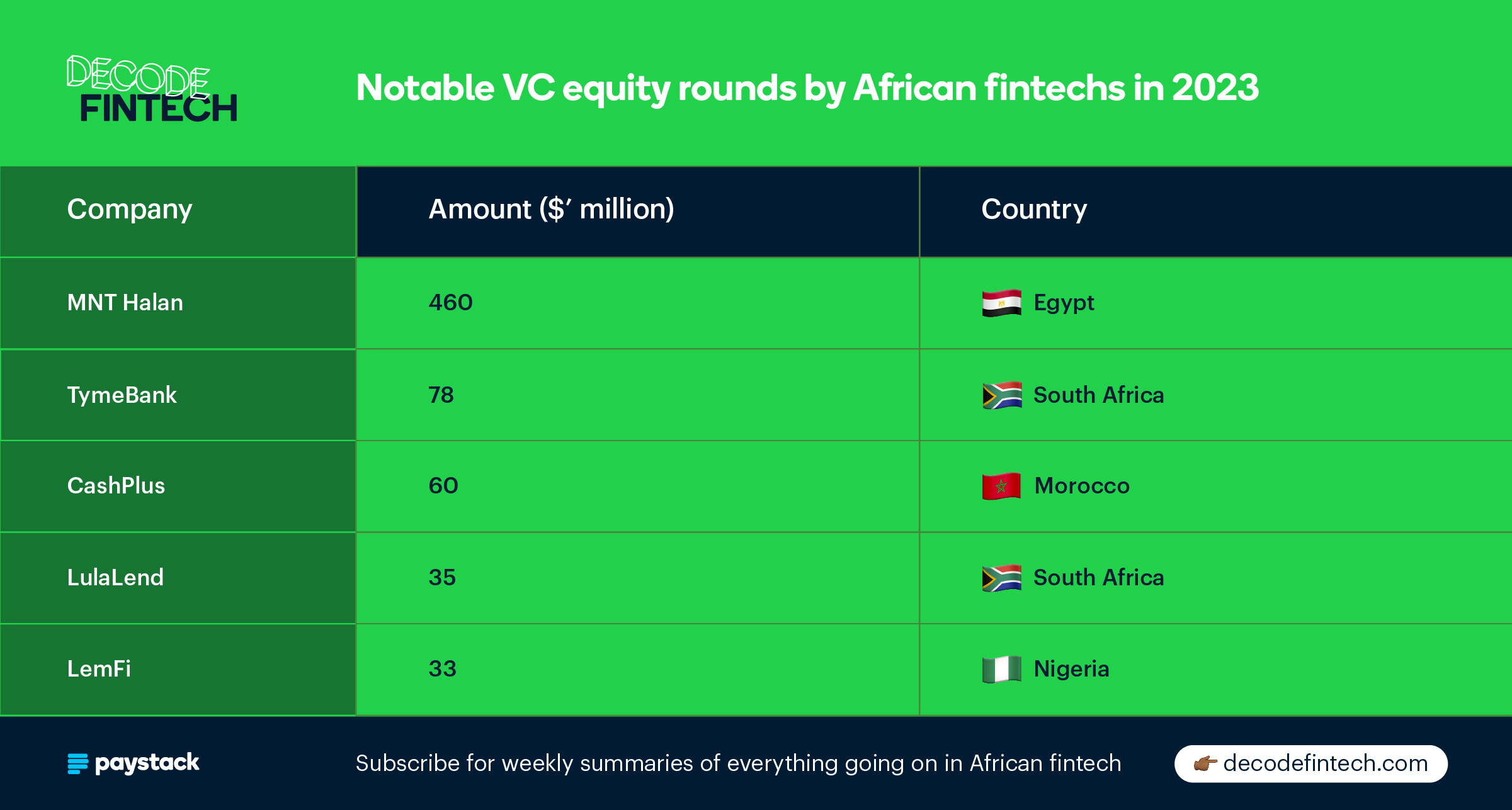

The last two years have posed significant challenges for venture capital (VC) investments into African startups, continuing a trend we highlighted in our 2022 African fintech review. Last year, the value of VC investments into African fintechs declined by 41% compared to the previous year. According to Briter Bridges, total funding to African tech startups hit $2.9 billion in 2023, a 39% decline from 2022.

Despite this decline, some African fintechs have shown remarkable resilience, continuing to make critical changes to ensure the survival of their business in an uncertain funding environment.

List of notable VC equity rounds by African fintechs in 2023

Some fintechs like Zazuu and Lazerpay faced the tough decision to close their doors due to a lack of funding, while others explored options such as hiring freezes, salary cuts, layoffs, pivots, pricing increases, and shuttered product lines.

For fintechs that ceased operations for other reasons, financial constraints often revealed underlying issues like mismanagement or flawed business models. Fintechs currently struggling to generate sufficient revenue for their operations or growth are seeing their respective runways fast approaching critical levels. With external funding still scarce or internal cash flow negative, many fintechs will have to explore even more severe changes to ensure their survival.

Notable African fintech shutdowns in 2023

In addition to pursuing mergers and acquisitions, which offer interesting benefits like expanded customer bases, enhanced technological capabilities, and improved market positioning, African fintechs are increasingly turning to debt funding as a viable alternative.

Debt financing can provide the necessary capital without diluting ownership, making it an attractive option for fintechs looking to maintain control while securing funds. However, it’s important to note that the lion’s share of this debt capital has been channeled towards digital banking and lending startups, as these segments often present business models and cash flow profiles best suited for debt financing.

Notable debt rounds by African fintechs in 2023

Boost your startup’s growth with Paystack

Scale your tech startup with fundraising support, tool discounts, priority technical support, and more!

→ Contact our Startup Programs teamIt will be interesting to see how African fintechs navigate and innovate within these constraints to not only survive but potentially get ahead. While constraints limit options, they can also serve as a catalyst for businesses to think more creatively. Despite the anticipated challenges, there’s a promising outlook for those fintechs ready to seize this period as an opportunity to reinvent their strategies and emerge stronger.

Inflation and currency depreciation driving changes in fintech supply chains

African fintechs continue to grapple with the dual challenges of consumer inflation and local currency depreciation across key markets, including Nigeria, Kenya, and Egypt. In 2023, these currencies weakened significantly, a shift that, coupled with surging food and energy costs, has affected vital fintech metrics like consumer spending and loan repayment rates.

While countries like Kenya and Egypt saw some currency appreciation earlier in the year, underlying macroeconomic weaknesses will affect long-term recovery. Nigeria, which has seen oil revenues and foreign investments falter, has removed subsidies for fuel, power, and foreign currency. Removing these subsidies affects consumer purchasing power and is forcing businesses to rethink existing models of consumer spending in one of Africa’s biggest economies.

Inflation rates in December 2023

African fintechs are deeply interconnected with the global market, relying on a mix of imported resources like capital, cloud services, card chips, and POS terminals, as well as globally priced costs like expert talent and transaction fees. In an ideal scenario, fintechs would balance their scales by either marking up local prices or scaling their operations to ensure that their local earnings keep pace with the mounting global expenses and inflationary pressures.

However, as we highlighted in previous editions of our newsletter, regulatory frameworks and competitive forces particularly constrain the pricing of financial products, significantly limiting the extent to which financial institutions can revise customer charges.

We anticipate that fintechs will tweak their approach by starting to charge for services that used to be free or offered at minimal cost, while also localizing costs to match revenue. This means they’ll be looking more at getting funded in local currency by getting listed on local stock exchanges or taking out local loans. This also means leaning towards working with local suppliers and tech partners for key services and rethinking hiring overseas talent.

When local alternatives fall short in availability or reliability, we’re bound to see some disruption to product offerings that rely on those crucial inputs. For example, the surge in POS terminal costs – discussed in Issue 182 of the Decode Fintech newsletter – has pushed agency banking providers in Nigeria to either scale back, pivot into merchant acquiring, or offer non-card options to agents.

The key question is determining which business models and supply chains will adapt and how they’ll navigate the ongoing impact of these macroeconomic shifts.

Get more stories like this

Subscribe to Decode Fintech for weekly summaries of what’s going on in African fintech.

→ SubscribeIncreased adoption of non-card payment methods for merchant payments

African consumers have long favored mobile money and bank transfers for peer-to-peer payments, while cards have been the go-to for commerce. But we’re now seeing more innovations that make wallets and bank accounts work better for merchant payments.

In 2022, card payments made up 54% of non-recurring transactions processed across all Paystack markets. In 2023, the percentage gradually dropped to 25% by December, with bank transfers and mobile money taking over the bulk of the transaction volume by year's end.

Explore Paystack 2023 in review

Bank Transfer was the most popular channel on Paystack in Nigeria in 2023. For more stats about Paystack’s 2023 performance, check out our 2023 in Review.

→ Explore Paystack 2023 in reviewAs we’ve noted before, the high cost of card processing fees and the expense of importing payment terminals and smart chips have pushed merchants and financial service providers toward more affordable, locally priced payment options. Additionally, consumers have shown a strong preference for affordable, familiar, and mobile-friendly payment methods, accelerating the shift away from card payments.

With growing interest in open banking and new developments like the introduction of consumer direct debit in Nigeria and standing orders by M-PESA, we expect these alternatives to surpass card payment experiences in 2024.

Tricky regulatory and political climate ahead

While some regional alliances and objectives exist, fintech regulation across Africa remains highly fragmented. Financial regulators in different countries are advancing at varying speeds and sometimes in conflicting directions. Given the challenges facing fintechs, the role of regulators as arbiters of compliance, protectors of consumer interests, and enablers of ecosystem growth has never been more critical.

A notable example of clear policymaking clashing with confusing enforcement is seen in Nigeria, where the Central Bank of Nigeria (CBN), following a personnel restructuring, released new guidelines for financial institutions regarding interactions with cryptocurrency companies. However, despite these regulations, Nigerian authorities have been cracking down on crypto firms accused of currency manipulation and other illegal activities.

The CBN has been active beyond the cryptocurrency space, introducing new regulations covering agency banking, contactless payments, and open banking. Similarly, other African countries have released updated guidelines, such as virtual assets in Namibia, and mobile money in Ethiopia.

Zooming out, African fintechs should also keep a keen eye on new policymaking directions driven by changing economic and political situations across the continent. In addition to inflation and currency depreciation, key African fintech markets like Nigeria, Egypt, and Kenya are grappling with mounting debt. Countries like South Africa have also recently changed leadership, and Ghana, by way of its elections, will be doing so in December.

We’ve already seen how an aggressive drive for tax revenue and new economic policies can affect fintech fortunes. In Nigeria, the CBN’s policies on new banknotes and cash withdrawals at the beginning of 2023 drove more Nigerians towards digital payments. The newly elected Nigerian government also removed fuel and foreign exchange subsidies which affected business and consumer spending. Over in the east, Kenya’s increased tax oversight on mobile money transactions has reportedly driven more Kenyan SMEs to prefer cash payments.

Ultimately, African fintechs must contend not just with dwindling cash reserves but also with emergent and uncertain policies that affect their businesses in new and unpredictable ways.

Get more stories like this

Subscribe to Decode Fintech for weekly summaries of what’s going on in African fintech.

→ SubscribeMigration’s impact on talent, remittances, and fintech expansion strategy

African technology workers are on the move. Explosive population growth, tightening economic conditions, and rising political instability are among the factors driving an exodus of African talent seeking better opportunities in developed, high-income countries.

Some of this migration is within the continent to emerging tech hubs like Kigali and Nairobi but most of these technology and business workers are setting their sights outside the continent, intending to earn globally competitive salaries from large tech companies or well-funded startups. Countries like the United Kingdom and Canada have spun up residence programs to take advantage of this shift.

Until Artificial Intelligence takes all our jobs, fintech products will still need to be built by people. There is little public data, but informal conversations with founders reveal that employee attrition from fintechs is already affecting key processes, including recruitment, product delivery, and partnership discussions. Facing fundraising and revenue challenges, many fintechs are losing leverage in hiring and retainment discussions and might struggle to acquire and retain experienced local talent as these limiting conditions persist.

The implications of brain drain for fintechs are not just disruption to business operations, but a dip in product experience for customers and a loss of critical context needed to avoid old mistakes and navigate a growing ecosystem.

That said, some fintechs are taking advantage of these migratory shifts. One positive effect of African migration has been growing foreign remittances into Africa from foreign workers. According to the World Bank, $53 billion in foreign remittances flowed into African countries in 2023 through formal channels.

Most remittances into the continent are either through costly legacy players or informal channels. Fintechs like LemFi, NALA, and Flutterwave’s Send have emerged or evolved to provide faster, cheaper, and more seamless remittance experiences for Africans.

Average remittance costs by region: cash vs digital services

Beyond just giving fintechs access to needed foreign currency liquidity, consumer remittances are also a first step towards a bigger expansion strategy. Modern financial plumbing that enables cross-border trade and money movement for entire economies and businesses will likely start with smaller pipes built for people to move money within and outside the continent.

As fintechs continue to face challenges within their operating environment, there might be solutions that exist outside of those borders.

But even if fintechs capture the financial opportunities, the tech talent issue remains a challenge. Startups dedicated to training tech talent have emerged, such as AltSchool Africa, ALX, and TalentQL, exploring internship and graduate trainee programs to broaden their talent pipelines.

However, the challenge isn’t just about hiring; it’s about retention. While a slowdown in the global tech job market has temporarily eased pressures for African startups, the long-term trend shows experienced professionals still seeking opportunities abroad.

Startups need to adapt by anticipating shorter employee tenures and overhauling their cultural and operational systems. This means expanding hiring pools for junior talent, investing in thorough documentation, standardizing employee development processes, and perhaps most importantly, creating a great work culture and environment for local talent.

Ultimately, it would be a significant setback if the innovation and ambition of African fintech were stifled by a lack of experienced and motivated professionals willing to commit to the mission. Any investment made towards retaining talent would be well worth it.

Boost your startup’s growth with Paystack

Scale your tech startup with fundraising support, tool discounts, priority technical support, and more!

→ Contact our Startup Programs teamOther themes and trends

Beyond the major themes above, several other notable trends are likely to shape the remainder of 2024.

Payment fraud

Payment fraud remains a significant challenge for both fintech operators and regulators. Despite advances in digital identity verification, losses due to fraud persist. The explosive adoption of mobile wallets and agent networks has also made these channels attractive targets for fraudulent activities.

According to NIBSS (Nigeria Inter-Bank Settlement System), digital payment fraud losses increased by 23% to NGN 17.7 billion in 2023, with mobile and point-of-sale (POS) channels recording the highest losses.

Artificial Intelligence and Machine Learning

Large Language Models (LLMs) have gained significant traction globally. African fintechs already use machine learning for identity verification, fraud detection, and loan underwriting. We expect these new AI Advancements to enhance products and back-office operations like support and compliance.

Crypto adoption

Interest in crypto is growing, particularly with the adoption of stablecoins and layer-2 blockchains for identity and other applications. African fintechs increasingly use crypto solutions for cross-border payments. While regulatory bottlenecks exist in markets like Nigeria, South Africa has introduced new licenses and regulations that may drive adoption.

Digital transformation

The transformation of payment and banking processes continues across both formal institutions and informal businesses. At Paystack, we’ve observed merchants in consumer goods, logistics, and even oil and gas shifting toward electronic payments. For instance, Chowdeck, a leading logistics and food delivery company in Nigeria, processed almost N2.5 billion in monthly volume without offering payment on delivery. Cab drivers and traders are increasingly comfortable accepting bank and mobile money transfers. We expect this shift to continue across markets as the year progresses.

As the year progresses and African fintechs navigate the evolving landscape, they'll need to continue adapting to the challenges posed by some of the trends mentioned above. However, despite hurdles like economic uncertainties and the ongoing talent migration, fintech on the continent remains a hotbed of innovation, poised to push economic growth and financial inclusion across the continent.

The rest of the year will be crucial for fintechs to reassess their strategies, embrace resilience, and seize the opportunities presented by the rapidly evolving ecosystem.

And as always, Decode Fintech will continue to be your trusted guide in the African fintech landscape through our long-form commentary.

If you’d like to share interesting fintech news happening in your part of the continent (or share news from 2024 we missed), kindly shoot us a message at [email protected]. We look forward to hearing from you!

Get more stories like this

Subscribe to Decode Fintech for weekly summaries of what’s going on in African fintech.

→ Subscribe