How NIBSS Instant Payment (NIP) powers Nigeria’s digital economy

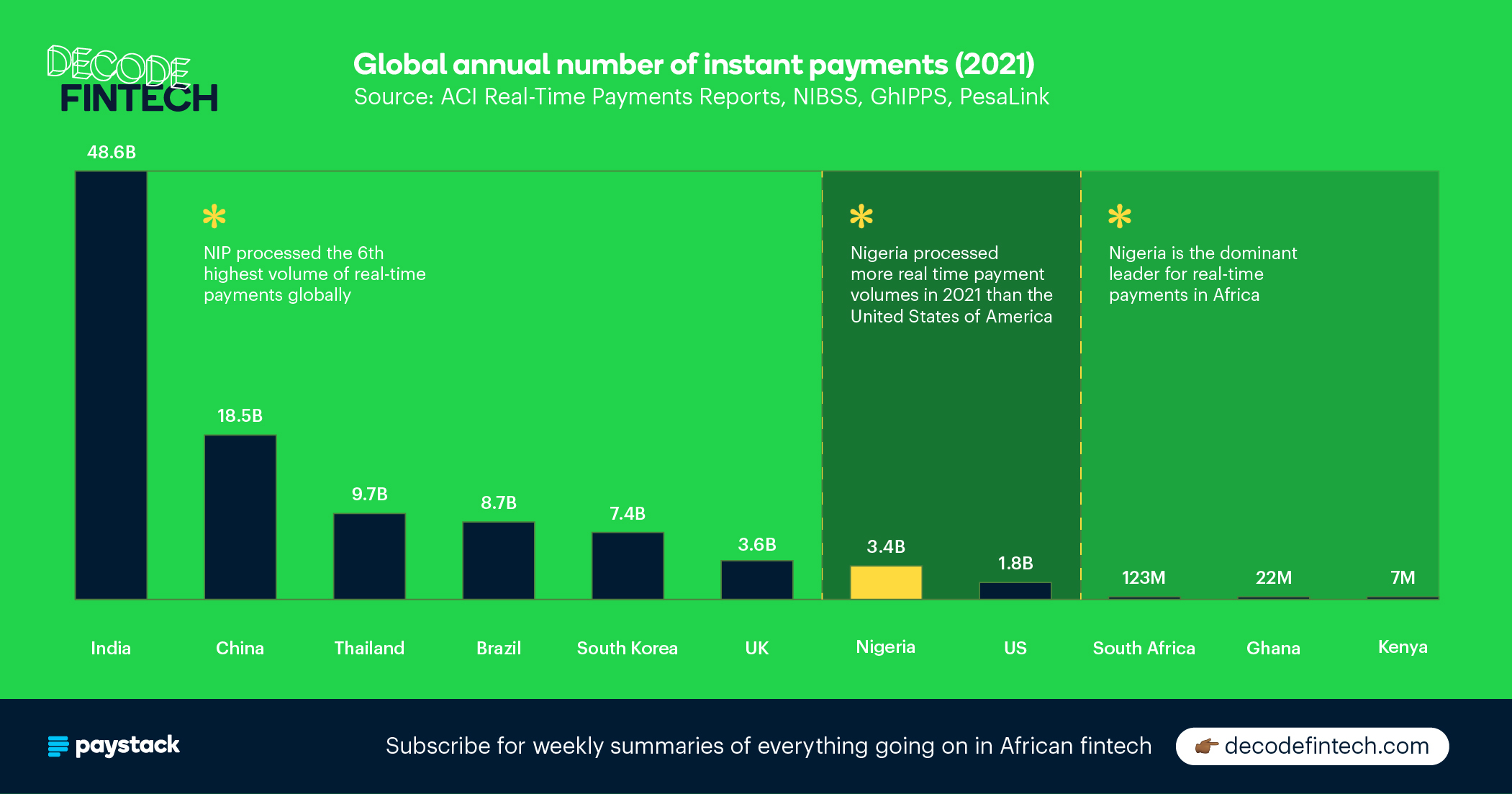

NIP is the sixth largest real-time payments system in the world, ahead of the US, and catalyzed the explosive growth of Nigerian fintech innovation. How did this happen?

Instant digital payment networks support trade and value exchange within and between countries worldwide. In Nigeria, one of those intricate systems is NIBSS Instant Payments (NIP), a payment service used by banks and other financial institutions to power real-time bank transfers for customers and businesses.

NIP processes billions of dollars every day, and is the largest instant payments service in Africa. In fact, annually, NIP processes more transactions than several payment systems in more developed economies. Beyond the sheer volumes that NIP processes, it has also been critical to the growth of financial innovation in Nigeria.

More and more, the Nigerian economy is moving at ‘NIP-time’ - payments are so fast, they can sometimes be faster than the time it takes to read this sentence. Chances are when transfers between two Nigerian banks happen via USSD, mobile money, or an internet banking portal, the payment is processed by NIP.

In a previous article about MTN’s MoMo PSB, we noted NIP’s critical role in the growth of fintech in Nigeria. In this article, we’ll dive deeper into the rapidly growing instant payments service, exploring its history, how it works, why it matters for digital payments in Nigeria, and why other African countries looking to accelerate their digital economies might want to consider building a similar solution to increase the velocity of money.

Need For Speed: Why does NIP matter?

In Nigeria, customers still largely prefer to make payments for low-value in-person transactions with cash. Both the transaction cost to the payer and the settlement time for the payee is usually zero. The time it takes for funds to be available for the recipient to use (settlement time) is particularly important to merchants and customers. This immediacy of value exchange instills a high level of trust in cash-based transactions, and is one of the contributing factors to sustained cash adoption in Nigeria, especially for in-person transactions.

The benefits of cash payments though, usually decline and sometimes disappear when the transaction amounts and distance between transacting parties increases. For domestic remittances and local trade between cities, it can become expensive and even unsafe to move cash, especially in large sums. The settlement time for these kinds of transactions is no longer zero due to the distance and time it takes to move the money.

On a larger financial scale, cash can be a significant burden for central banks and other financial institutions. In 2020, the Central Bank of Nigeria (CBN) reportedly spent ₦58.6 billion (about $141 million) to print cash worth ₦1.1 trillion (~$2.5 billion) in value. This means that as of 2020, the cost of printing naira bank notes represented 5.5% of the total cash value, not including the cost of vans, security personnel, vaults, and other physical infrastructure needed to move and manage that volume of cash.

Digital payment systems looking to disrupt the widespread use of cash have to solve its logistical issues while replicating its benefits. Many electronic payment systems try to solve problems of reliability and cost, but lack the benefit of immediate settlement times. Fast payment systems like NIP bridge this gap by reducing settlement times to near-zero.

The ability of NIP to reliably send and receive money instantly from any bank account at any time has had a significant impact for consumers, businesses, and the Nigerian financial system as a whole.

- The instant nature of NIP payments can be very critical for time-sensitive payments like rent, bills, and health emergencies. For millions of Nigerians with low and irregular sources of income, having immediate access to funds after providing a service can be a literal life-saver, especially when loans from friends and family are not readily available.

- For businesses, instant NIP payments reduces the amount of working capital needed for daily operations. The faster a business can access revenue from customers, the less it has to rely on cash reserves or interest-bearing credit facilities to pay suppliers. According to ACI Worldwide, NIP helped Nigerian businesses save an estimated $296 million in 2021. This instant availability of funds flows into existing supply chains, increasing the velocity and expanding the surface area of commerce in the economy.

- Guaranteed instant payments help more customers and businesses trust digital financial services, which leads to greater adoption and a drastic reduction in cash reliance. This directly benefits banks and the government. The NIP trends in the last five years show a steady decline in the average value of an NIP bank transfer, even as volume and value are increasing significantly. This indicates that the use of NIP bank transfers for every day, lower-value transactions is increasing.

- Instant digital money movement makes it possible to build popular, innovative financial products offered by fintechs and banks. Fintech solutions - including savings, investments, insurance, and credit products - embed instant disbursements into their core product offerings, and the promise of instant payouts makes the value proposition of these products a lot more attractive to prospective customers.

Get more stories like this

Subscribe to Decode Fintech for weekly summaries of what’s going on in African fintech.

SubscribeA brief history of NIP

Bank transfers in Nigeria were not always as easy or instantaneous as they are today. Before NIP, customers often queued in banking halls, filled out lengthy forms, or presented cheques to send and receive money.

In 1993, the Nigerian Bankers Committee incorporated NIBSS, and amongst other things, the agency was tasked with centralizing payment and settlement activities among banks and other financial institutions. This involved a manual and time-consuming process of clearing cheque payments and the settlement of positions between banks.

In 2004, NIBSS launched the NIBSS Electronic Fund Transfer (NEFT), an improvement to the existing clearing house system, which allowed for automated and electronic clearing and settlements. It wasn’t the first widely available fund transfer service. Interswitch and eTranzact, launched in 2002 and 2003 respectively, were already working to provide electronic payment services to banks. NEFT was available to all major banks and saw strong adoption, but it still wasn’t real-time, as transfer instructions from customers had to be batched together and processed during limited settlement windows in the day.

The Central Bank of Nigeria (CBN) also provided inter-bank services directly, first through the Central Inter-Bank Funds Transfer Service (CIFTS) and eventually through the Real-Time Gross Settlement System (RTGS). While RTGS provided real-time fund transfer services, it was relatively expensive, and mostly reserved for high-value transactions including settlements between banks.

Get more stories like this

Subscribe to Decode Fintech for weekly summaries of what’s going on in African fintech.

SubscribeIn 2005, the Central Bank of Nigeria held a recapitalization exercise which had several effects on the Nigerian banking system, including mergers between several banks. A year after this exercise, the CBN, formally appointed NIBSS as the National Central Switch (NCS), and was mandated to connect all CBN-licensed banks, switches, and mobile money operators in Nigeria, and to ensure payment instruments, networks and systems were interoperable. This was a pivotal step towards driving the adoption of cashless payment methods. It would also lay the groundwork for the introduction of NIP.

NIBSS Instant Payments (NIP) was launched in 2011 by NIBSS to electronically facilitate real-time bank transfers. In that same year, the CBN directed all banks to adopt a standardized 10-digit account number format known as Nigeria Uniform Bank Account Number (NUBAN). Up until then, account numbers had varying lengths and formats. This introduction of a standard NUBAN format made it easier to validate electronic payments and routing.

The Central Bank of Nigeria also made it necessary for future categories of financial institutions such as mobile money operators and payment service banks to connect directly to NIP and were interoperable with the rest of the Nigerian financial system.

With NIP, customers had access to an electronic transfer service that could reliably and cheaply perform bank transfers without having to queue in banks.

Sell more online

Paystack has all the payment tools you need to start and scale your business.

Create your free accountHow does NIP work?

On a fundamental level, a digital payment involves a series of messages, sent securely and electronically through trusted agents, that execute a change in the financial records of two or more parties. A bank transfer is similar to a text message between banks, and less about the movement of bullion vans full of actual cash.

If payments are messages, NIP is a central messaging platform that banks and other financial institutions use to send payments and execute instructions to each other for a fee. Payment systems are designed differently, which explains why not all payments are instant. Once a bank transfer is initiated by a sender, it has to be cleared, then settled irrespective of the payment system. Clearing is the process of sending, reconciling, and confirming payment requests, while settlement is the process of making the funds available to the recipient.

To appreciate how NIP works requires that one understands the important concept of how money moves between banks.

Most people assume that when someone sends money from Bank A to Bank B, a bullion van full of cash moves from one bank to another. This is not what happens. In reality, what the money movement looks like is that one bank will log a debit in their financial records, while the other bank logs a corresponding credit in their financial records.

In legacy non-instant payment systems, the clearing process (the process of reconciling payment requests) does not happen in real-time. Instead, payment instructions are collated in batches and cleared at particular periods before settlement. These traditional payment systems also require the inter-bank settlement to occur before funds are made available to the recipient. This introduces delays, and as a result, bank transfers through these systems take hours or even days. These delays can vary depending on country and payment type: In Brazil, credit card transactions can take up to 30 days to get settled to the merchant.

Get more stories like this

Subscribe to Decode Fintech for weekly summaries of what’s going on in African fintech.

SubscribeFast payment systems like NIP, however, are designed differently. When a bank transfer is initiated through NIP, the payment request is immediately sent to the recipient’s bank and funds are made available to the recipient almost instantly. In between, several other steps such as confirming the account balance of the sender, and validating the accuracy of the recipient bank account happen very quickly. The settlement step between the banks is deferred to certain periods during the day. For these inter-bank settlements, banks have accounts in the CBN which NIBSS has access to and is able to offset using CBN’s Real-Time Gross Settlement System (RTGS).

By separating the high-level credit-debit instructions away from the inter-bank settlements, NIP can provide an instant payment experience for end-users.

Banks are not the only intermediaries for NIP-enabled bank transfers. Other financial institutions, such as mobile money operators and payment service providers, also leverage NIP to facilitate fund transfers for customers. These non-banks use application programming interfaces (APIs) provided by NIP directly or a commercial bank to perform these bank transfers. In addition, these non-banks have to partner with licensed commercial banks that have accounts with the CBN for the inter-bank step of the settlement process.

NIBSS also offers an NIP-enabled direct debit service where users can mandate their banks to debit a fixed amount from their bank account at a set time. Although this service is not as widely-used as the bank transfer service, it still sees some significant traction, especially for mobile payments.

Beyond transfers, NIP also provides important ancillary services, including a name enquiry service to confirm recipient bank details and a dispute resolution service for customer disputes. These solutions reduce errors and contribute to the overall efficiency of the NIP service.

Looking at the numbers: Everything, Everywhere, NIP

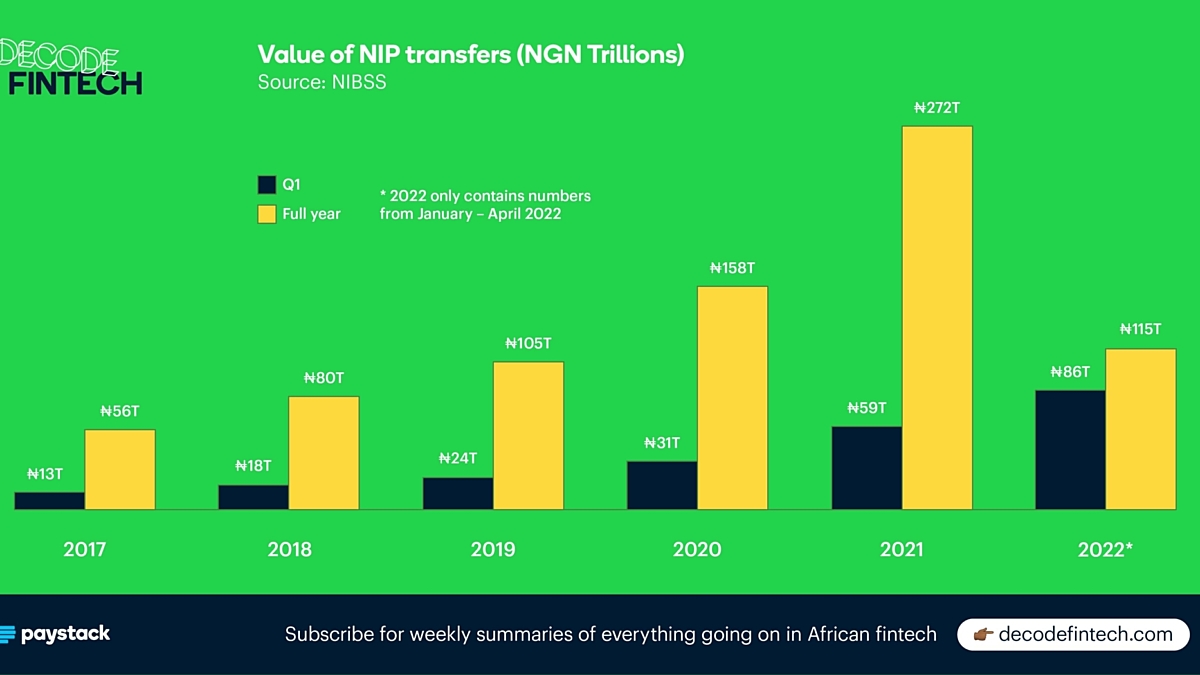

An analysis of the data on volumes processed by NIP as provided by NIBSS on their publicly available data portal gives us a clear sense of NIP's sheer scale and success; the numbers are staggering, to say the least.

In 2021, ₦272 trillion (~ $650 billion) worth of transfers were processed through NIP, a 72% increase from 2020. This is more than the total amount processed from 2017 to 2019 combined (₦224 trillion).

These numbers have continued to grow in 2022. In the first quarter of the year, NIP processed ₦86 trillion (~$204 billion), more than the amount processed in 2017 and 2018.

The number of NIP transfers tells a similar story of rapid growth. In 2021, 3.4 billion transfers were processed through NIP, a 71% increase from the previous year.

These numbers do not include intra-bank transfers (transfers within the same bank) or transfers through other payment platforms like NEFT or other payment switches. This suggests that the aggregate value of digital payments in Nigeria is much higher. If we compare NIP to other payment channels like NEFT, cheques, and POS, we’ll find that NIP is the dominant channel for payments in Nigeria.

While customers and businesses have directly benefited from NIP’s speed and reliability, banks and other financial institutions (OFIs) have also earned a lot from transfer fees. If we assume a conservative average transfer fee of ₦10, then financial institutions conservatively earned an estimated ₦34 billion (~$81 million) in gross transfer fees from customers in 2021. This figure is likely higher if we account for high-value transfers which incur a higher fee.

Zooming out, NIP is one of the leading instant payment services in the world. Nigeria is also one of the few countries in Africa with a national real-time payments service like NIP. Most African countries without a central real-time payments service have to rely on fintechs or telco-led mobile money operators for instant money movements.

Sell more online

Paystack has all the payment tools you need to start and scale your business.

Create your free accountBut what is behind this NIP success story?

A combination of speed, affordability, interoperability, and reliability made NIP the preferred channel for digital payments in Nigeria. Policy decisions by the CBN such as the consolidation of banks, the introduction of NUBAN account formats, and the aggressive push towards cashless payments, have also allowed NIP to scale from two banks at the time of launch to almost all banks and digital wallets.

But product superiority and regulatory backing don’t provide a full picture of the rise of digital payments in the last ten years. A couple of larger industry trends and macro-economic drivers further explain this astronomic growth.

Increasing mobile and smartphone penetration

Smartphones and overall mobile penetration in Nigeria have increased in the last decade. At the end of 2010, just before the launch of NIP, Nigeria had 89.3 million mobile subscriptions and a mobile penetration rate of 54%. More than a decade later, there are now over 200 million mobile subscriptions and almost 150 million mobile internet subscriptions in Nigeria.

Banks, fintechs, and now telcos (via payment service banks) have taken advantage of this boom in mobile and internet adoption to grow the use of digital payments. Almost every commercial bank in Nigeria offers a mobile app and internet banking portal for their customers to perform financial services. There are USSD-based banking services available that don’t require an active internet connection. These digital channels, which make it more convenient to engage in financial services, usually leverage NIP for inter-bank transfers.

COVID-driven acceleration of digital payments.

The COVID-19 pandemic led to lockdowns and disrupted global economies, including Nigeria. It however also drove the need for less contact between businesses and their customers, which increased demand for cashless payments. April 2020, the month where Nigeria was in complete lockdown, saw the value of NIP transfers dip to a two-year low of ₦7 trillion. But the months after the lockdown saw volume sharply pick up and continue to rally even after the number of COVID-19 cases reduced.

This trend of COVID-driven increase in cashless payments was not limited to bank transfers. Paystack saw increased merchant signups and customer activity across all payment methods after the April 2020 lockdown, and while businesses have opened up, it appears newly acquired customer preferences for online payments have stuck.

Sell more online

Paystack has all the payment tools you need to start and scale your business

Create your free accountTransformation of business models and payment processes

Many Nigerian industries have leveraged the speed of NIP transfers to significantly improve money movement processes or design entirely new ones.

In the last five years, neobanks and fintechs offering agency banking, digital savings, investments, credit, and other financial services have risen significantly. Users are typically assigned virtual bank accounts to deposit into a wallet, and are also allowed to withdraw funds or send money to other bank accounts. The ability to deposit and disburse in real-time, usually through NIP-enabled providers like Paystack, has gone from being a market differentiator to a basic expectation from consumers.

These advantages are not only available to financial services. Industries like sports betting are leveraging NIP-enabled transfers to provide instant winnings to their customers. Eventually, many more Nigerian businesses will identify points in their workflow that involve money movement, and will implement ways to make this faster through NIP.

The evolution of bank transfers for web payments.

Zooming out, there has been an interesting modification of bank accounts for customer-to-business payments in the last few years. To be clear, customers have always been able to make bank transfers into corporate accounts and this form of payment has become increasingly popular in social commerce and formal retail.

But at very high volumes, bank transfers into a single corporate account introduce tricky reconciliation and payment confirmation challenges. Payment providers like Paystack have been able to design and implement payment experience user interfaces that are similar to debit card payments but actually leverage bank accounts. Customers paying on a website can now pay into temporarily available bank accounts at the point of checkout. Because these payments have to be made in a limited time, the bank transfers are usually performed through NIP-enabled digital channels.

This is a big deal because bank accounts are very ubiquitous in Nigeria. Enabling bank transfers for web payments expands the potential market for eCommerce with a tool that people trust. The Pay with Bank Transfer option on the Paystack Checkout has seen tremendous adoption since its launch.

These factors are some of the key drivers of the adoption of NIP-enabled transfers in Nigeria and we expect this to continue. With the increase in P2P cross-border remittances, we should expect the growth of NIP and overall digital payment volumes to continue.

The big payments opportunity: the rise of new rails

Despite NIP’s dominance, there’s still a wide surface area of payments that NIP doesn’t touch. Additionally, the reliance on NIP by financial services providers presents a concentration risk that becomes apparent in the event of a downtime. NIP downtimes are quite rare but when they do happen, local money transfers between banks and withdrawals from financial products can become critically impacted.

As mentioned already, NIP is not the only available fund transfer service in Nigeria. There are alternative platforms like Interswitch, eTranzact, and NIBSS-managed NEFT that also process trillions of naira every year. In addition, intra-bank transfers are processed within the bank and don’t usually require an external switching provider.

Fintech disruptors like Pocket (formerly Abeg), FairMoney, OPay, and PalmPay are also building closed-loop multi-sided networks for customers and businesses. These fintechs are working to capture a sizeable percentage of existing payment revenue through improved customer experience and value-added services like savings, lending, insurance, and remittance. Crypto startups are also building new borderless payment rails for money movement, and might rely less on fiat infrastructure in the future.

Despite these alternatives and the potential for aggressive competition, the opportunity for all players is endless. Many customers and businesses still prefer cash and operate outside the ambit of the formal financial system. Onboarding and convincing these users will require investments from multiple stakeholders.

In our last article about the MTN MoMo PSB, we wrote about the network effects of acquiring new users into a payment network. As these customers and businesses are provided with digital financial tools, we should expect even more volumes from NIP and its many alternatives.

Understanding MTN Nigeria’s PSB License

In our first Decode Fintech article, we explored how MTN’s PSB license could change the face of financial services in Nigeria, and what this might mean for customers, fintechs, and financial inclusion in Nigeria.

Read the articleNigeria’s economy moves at the speed of NIP

NIP helped accelerate the growth of digital payments in Nigeria. Customers, businesses, financial institutions, and the Nigerian economy benefit immensely from the availability of instant money movements.

If a country’s pace of financial innovation is directly indexed to the shortest time it takes to move money electronically, then any investment that an African economy makes to accelerate that speed, is worthwhile.

NIP-enabled instant payments are not a silver bullet for creating a cashless economy. There are still complex obstacles to reducing cash usage and introducing more consumers to formal financial services. NIP remains the closest and most successful substitute to cash, and as regulators and operators continue to drive financial inclusion, instant payments will continue to play a big role in that transition to the digital economy, beyond Nigeria and across the continent.

Cash is still king, but if you pause to look carefully, you will notice that the future is already here.

Continue the conversation at Decode Fintech Round Table

We hope this deep dive has been helpful in understanding the ways in which NIP is contributing to the rise of digital payments and powering the economy in Nigeria.

To continue the conversation, join us on Wednesday, August 31, 2022 for this month’s Decode Fintech Roundtable where we’ll share more on the impact of instant payments in Nigeria. Reserve your free seat here!

A correction was made on Feb. 13, 2023:

An earlier version of this article misstated the number of transactions processed by the UK. The number is 3.6 billion, not 3.4 billion. The article also misstated the number of transactions processed by Nigeria's NIP. The number is 3.4 billion not 3.7 billion. As a result, the article misstated that Nigeria's NIP processed more transactions than the UK and the statement has been corrected.