Understanding MTN Nigeria's Payment Service Bank (PSB) License

A deep dive into how MTN’s PSB license could change the face of financial services in Nigeria, and what this might mean for customers, fintechs, and financial inclusion in Nigeria

On April 11, 2022, the Central Bank of Nigeria granted MTN Nigeria final approval to operate a Payment Service Bank. A little over a month later, Nigeria’s largest telecommunications provider launched its MoMo Payment Service Bank (PSB) to the public, allowing its Nigerian customers create accounts, pay bills, send and receive money, and more - services which have been available to customers in other countries for years.

MTN has a large mobile money business in several other markets across Africa, and is looking to replicate this in Nigeria where its voice and data services are more popular.

Although this license seems to change things significantly, it’s not without its limitations. In this article, we aim to break down what kinds of services this license allows MTN Nigeria to offer, and why this matters for customers, businesses, and other fintechs.

Get more stories like this

Subscribe to Decode Fintech for weekly summaries of what's going on in African fintech.

Subscribe

A brief history of MTN’s financial services

In 1994, only three years after the first GSM call was made in Finland, MTN was founded in South Africa as M-Cell. Upon achieving national success, it expanded across Africa, targeting markets looking to open up their communication industry to private operators.

MTN Nigeria launched in 2001, and in over 20 years, MTN has expanded coverage to most areas of the country, thanks to long term investments in communication, infrastructure, and improving service delivery. It also helped that since its early days, MTN has invested in a network of micro-agents and wholesalers who register customers and sell prepaid airtime, bringing its services close to most communities.

Today, MTN has over 75 million mobile subscribers in Nigeria and 272 million subscribers across 19 countries in Africa, making MTN the largest telecom operator in Nigeria and one of the biggest operators on the continent.

At the time of MTN’s launch in Nigeria, most African countries had expensive and inadequate banking and payments infrastructure which made it hard for customers to move money around. As more people began to use mobile phones, and more mobile networks reached a large customer base, operators and regulators explored using the existing mobile distribution to provide financial services.

Mobile phones presented an opportunity to offer customers a “bank in their pocket,” an easier and affordable way to provide basic financial services like deposits, withdrawals, transfers, bill payments, and credit. Along with a hive of ever-present physical agents, financial services suddenly became within reach.

Before Safaricom popularized telco-led mobile payment in Africa with the launch of M-PESA in 2007, MTN was already exploring ways to provide financial services through mobile phones. In 2005, MTN South Africa partnered with Standard Bank Group to launch MTN Mobile Money, a SIM-based mobile banking service.

The service was branded and distributed by MTN but was a division of Standard Bank Group which provided the actual financial services.

M-PESA’s success in Kenya saw more telcos expand mobile money services into other markets. This included MTN, which began to offer its mobile money service in some of its existing African markets like Cameroon, Ghana, Rwanda, and Uganda. It partnered with banks and regulators, and leveraged its strong brand presence and agents to scale quickly in these markets.

By 2021, MTN Mobile Money was present in about 15 countries with 56.8M customers completing 10 billion transactions worth about $240 billion.

In Nigeria, however, the journey to replicating this success has been complicated.

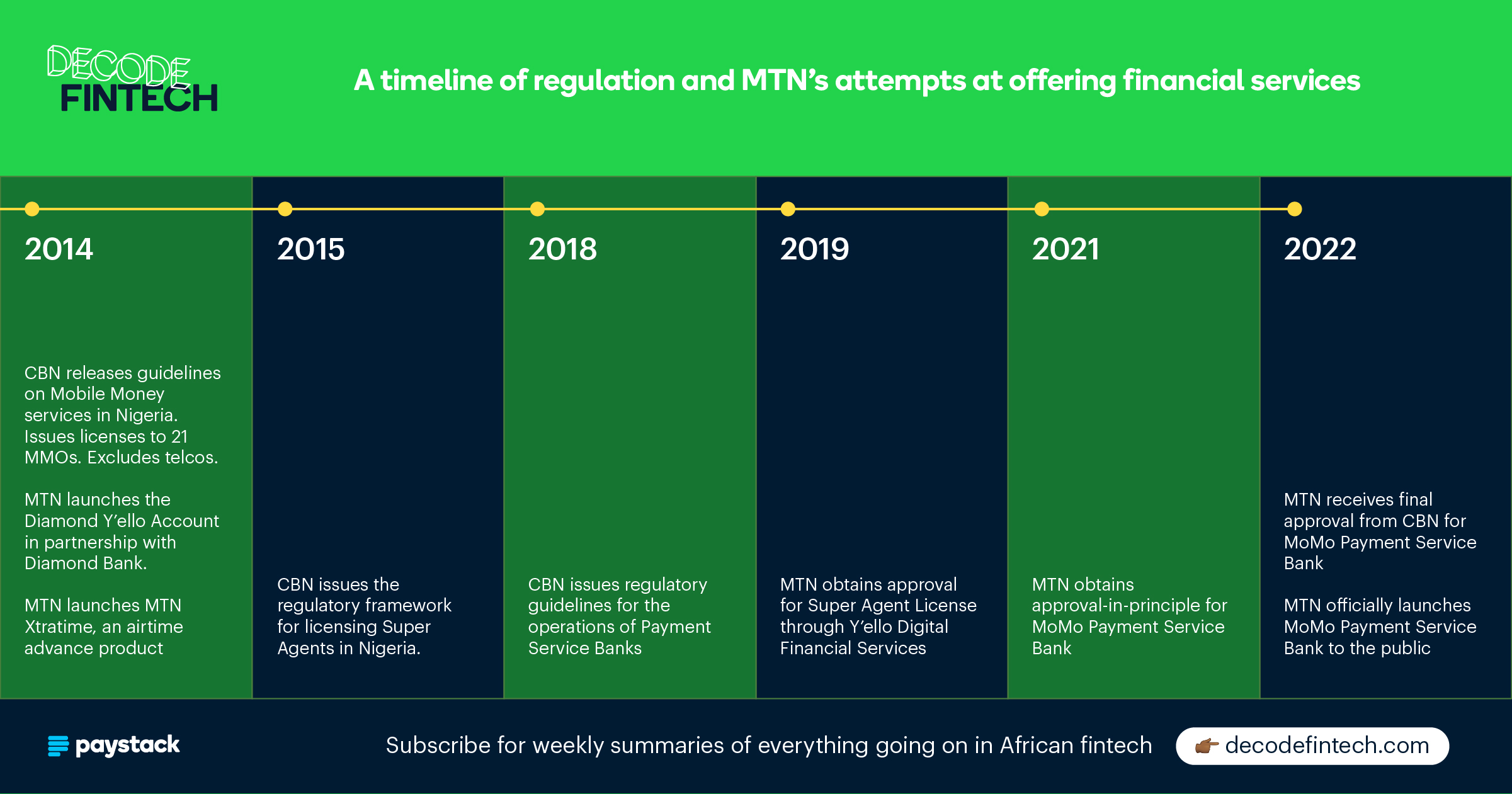

Throughout the last decade, the Central Bank of Nigeria made policies to reduce cash usage and strengthen financial inclusion, and in 2014, it introduced the Mobile Money Operator (MMO) license which allowed banks and other financial institutions to provide mobile money services targeted at the financially excluded. Under the rules, MTN was only allowed to provide communication infrastructure, and could neither apply for the license nor offer the services permitted.

MTN partnered with banks, and one of the more popular partnerships with Diamond Bank (now part of Access Bank) led to the launch of Diamond Y’ello in 2014, a product similar to the 2005 offering with Standard Bank Group in South Africa. By dialing a USSD code, MTN subscribers could open Diamond Y’ello Bank accounts from their mobile phones, and perform basic bank activities such as making transfers, buying airtime, and paying bills. In that same period, many commercial banks started launching their USSD banking service. While MTN and other telcos did benefit from the adoption of these channels, most of the value was captured by the banks.

Also in 2014, MTN launched XtraTime, a service that allows its prepaid customers to borrow airtime on credit. This product has been very successful, making up a significant portion of MTN’s fintech revenue in Nigeria.

Five years later in 2019, the CBN granted Y’ello Digital Financial Services (YDFS), a subsidiary of MTN, a super-agent license which allowed MTN to partner with other financial institutions to offer MTN customers person-to-person (P2P) cash transfers and bill payments through a network of physical agents. In 2021, MTN Nigeria’s MoMo service added about 374,000 registered MTN MoMo agents and had about 9.4 million customers. By the first quarter of 2022, the number of registered agents had surpassed 800,000, with over 166,000 active agents.

Even with this early success, the super-agent license still had several limitations. For example, the license didn’t give MTN the power to hold customer deposits in digital wallets, and as a result, MTN couldn't provide a wider range of financial services or build a deeper relationship with its customers.

This is perhaps why this Payment Service Bank license seems to be the long-awaited ticket for telecommunication companies like MTN to offer financial services. But how true is this?

GO DEEPER: A History of Mobile Money in Ghana

In Season 2 of the Decode Fintech Podcast, we explored the history of mobile money in Ghana, one of the fastest growing mobile money markets in Africa. Listen to learn how this happened, and MTN's journey to building one of their most successful financial services product on the continent.

Listen to the episodeWhat does the PSB license allow MTN to do?

In 2018, the Central Bank of Nigeria introduced new regulatory guidelines for the creation of Payment Service Banks (PSBs) with the goal of driving high-volume, low-value customer deposits, savings, and remittances, particularly in rural under-banked regions. This PSB model was heavily influenced by India’s Payment Banks (PBs) which received global attention following their launch by the Reserve Bank of India (RBI) in 2014. These new banks were expected to drive financial inclusion in underserved regions.

Possibly recognising the inevitable role of mobile network operators in driving its financial inclusion targets, the Central Bank of Nigeria allowed the telcos to apply for the PSB license through subsidiaries. Since 2018, full PSB licenses have been granted to all four subsidiaries of the major mobile network operators in Nigeria (MTN, Glo, 9 Mobile and Airtel). Airtel Nigeria, which was the most recent recipient of the PSB license, also launched its SmartCash PSB on May 20, 2022.

With the new PSB license, MTN’s MoMo PSB can:

- Accept deposits from customers and small businesses

- Hold funds in an electronic wallet

- Invest in interest-bearing FGN and CBN securities and offer saving products

- Engage in different forms of local payments including merchant payments, bill payments, and person-to-person transfers

- Provide inbound remittance services

- Issue prepaid and debit cards

- Provide POS and ATM services

- Build a network of physical banking agents for deposits, payments, and withdrawals

According to MTN’s press release of the MoMo PSB launch, “by dialing *671#, customers can open a MoMo wallet, send money to any phone number in the country and pay their bills.” Given the full scope of activities available to PSB license holders, it's very likely that MTN will provide even more services to customers in the near future.

There are a number of ways MTN can take advantage of its existing brand affinity and distribution capacity to leverage and successfully unlock the full benefits of the PSB license. Let’s look at a few of them.

Accelerate customer acquisition and financial inclusion

According to EfInA, 61% of financially excluded Nigerians have a mobile phone. MTN can drive customer acquisition by leveraging its extensive and growing agent network to bring formal financial services to underserved users in rural and frontier regions. About 35.9% of the Nigerian population still lacks access to financial services, and MTN can provide that critical on-ramp to the financial ecosystem for these users. They can also gain new users by offering electronic wallets as device-agnostic USSD services and mobile applications. It is no surprise that the first version of the MoMo PSB is a USSD service, and is available on every network as stated in its press release. Moving beyond a closed-system, telco-based mobile money offering to multi-service smartphone apps has always been a key part of MTN's long-term fintech strategy.

Increase the average revenue per user of existing subscribers

Despite being MTN’s largest market in terms of overall revenue, MTN Nigeria’s average revenue per user (ARPU) in the fourth quarter of 2021 stood at only ₦2,088 (~$5), 25% lower than MTN South Africa’s average revenue per user of ZAR97 (~$6.3).

Digital data and fintech revenues increased as users’ behaviours shifted towards the internet and digital services, and voice revenues declined.

The new license can increase MTN’s average revenue per user in two ways:

- MTN can leverage its existing agents to provide financial services to customers and capture most of the revenue for each transaction. As noted in an earlier section of the article, because the super-agent license did not allow MTN to hold funds, MTN could only offer financial services through its agents, and only on behalf of other banks and mobile money operators. This meant that for each transaction a customer did, MTN had to share revenue with other financial institutions. Because the PSB license allows MTN to hold funds in an electronic wallet, this is no longer the case, and MTN doesn’t need to rely on partnering with banks and other financial institutions.

- MTN can potentially up-sell its expanded financial services offerings directly to its millions of subscribers through USSD, SMS, digital marketing, and other forms of promotion. By converting even a small percentage of existing users to active MoMo PSB wallet holders, MTN can earn added revenue from payment fees and gain interest on users’ deposits.

Facilitate merchant payments & ecommerce

The super-agent license was very limited in its scope as MTN could only provide its customers with bill payment services. With this PSB license, though, MTN digital wallets can become a source of funds for consumer-to-business (C2B) and business-to-business (B2B) merchant payments.

These payments can be made either through a direct transfer from the MTN MoMo PSB wallet to other wallets and bank accounts, or through a debit card issued to the wallet holder and tied to the user’s funds.

In the long-term, MTN can build a critical mass of both businesses and customers, and facilitate payments between both parties at almost zero marginal cost. This is a strategy that it has successfully executed in other African countries with $13.3 billion in gross merchandise volume (GMV) paid to about 785,000 active merchants in 2021.

Subscribe to Decode Fintech

Weekly summaries and analyses of what's going on in African fintech.

SubscribeReduce the cost of airtime distribution

Since most customers have their funds in physical or digital stores of value that MTN doesn’t control, MTN relies heavily on wholesale agent networks and other financial institutions to distribute airtime to customers. This means that MTN has to incur costs both in managing the scale of operations and paying out to these middlemen.

By becoming a store of funds itself, MTN users can top up their airtime directly from their digital wallet or relatively cheaper MoMo agents. Today, about 24% of MTN airtime sales in the continent are through MTN mobile money wallets, a number that is expected to rise now that MTN Nigeria has launched its PSB operations.

Offer remittance services

MoMo PSB is allowed to receive inbound remittances from outside the country into Nigeria, and convert that FX through CBN-authorized channels. Despite high remittance inbounds, Africa still suffers from cross-border money movement challenges which have made remittances beyond and within the continent quite expensive for the average user. Nigeria, in particular, is one of the largest recipients of remittance inflows with over $14.2B remitted in the first three quarters of 2021.

MoMo PSB can make remittances more accessible to their customers, by allowing direct remits into digital wallets, and by leveraging a network of distributed banking agents to reduce the distance traveled to obtain remittances. In the long term, MTN can build a cross-border super-network of its different mobile money services in African markets.

Sell more online

Paystack has all the payment tools you need to start and scale your business.

Create your free account

Limitations abound

Despite the possibilities, the PSB license comes with significant restrictions. According to the regulations, MTN’s MoMo PSB cannot:

- Directly provide loans or advances

- Underwrite insurance

- Accept and hold foreign currency deposits

- Engage in foreign exchange transactions except for the purpose of inbound remittances

- Accept alternative means of value like airtime as a means of payment

In addition to these limitations, 25% of physical activity must take place in rural areas with a high unbanked population as defined by the CBN.

The core business model for many traditional banks involves collecting deposits at low interest from customers and businesses, and using these low-interest deposits to offer higher-interest loans. The net interest income obtained through this usually makes up the bulk of the banking revenue. Because Payment Service Banks can’t offer credit, they’re limited to earning money on fees charged for payments, and interest earned from investing in the Central Bank and Federal Government securities like bonds and treasury bills. These might not be lucrative as most customer payments are low-amount transactions with capped fees, and have low take rates per transaction. In addition, income on investments in CBN and FGN securities are increasingly uncertain as annual average yields have continued to decline in recent years.

In effect, payment service banks will have to process a high amount and velocity of transactions while also figuring out how to offer market-competitive returns on customer savings and deposits.

These limited revenue options combined with the extensive up-front costs required to scale probably contribute to why earlier recipients of the PSB license have gained little traction. It also comes as no surprise that India’s Payments Banks from which Nigeria heavily borrows, are being allowed to seek lending licenses after years of operational losses.

The requirement of having 25% physical activity in rural and frontier regions will also affect MTN’s payment service bank because the local nature of agency banking means that financial success is reliant on the level of economic activity within a particular location. In frontier regions with relatively non-existent digital infrastructure or economic activity, agents and operators are likely to struggle with earning a profit or sustaining operations.

Existing banking models are only viable for 51% of the Nigerian adult population because a significant number of Nigerians still lack power connectivity, cell coverage, and financial infrastructure. This is perhaps why many existing mobile money providers tend to concentrate in urban and semi-rural locations. To drive adoption in frontier regions, MTN might have to use significant interventions like marketing, education, and subsidies.

The implicit limitation on remittances is another restriction MTN will have to navigate. While PSBs are allowed to engage in inbound remittances and sell the foreign currencies from the remittances to authorized dealers, in recent years, the CBN has aggressively put out FX policies to strongly protect the naira against foreign currency devaluations. One of those policies requires FX remittances to customers to be received directly without any intermediate currency conversion. This presents a difficult situation for PSBs as they are not allowed to hold foreign currency deposits.

Get more stories like this

Subscribe to Decode Fintech for weekly summaries of what's going on in African fintech.

SubscribeWhile it is quite easy to confuse MTN’s MoMo PSB for mobile money, they are actually different categories of financial institutions by law. In the table below, we consider how these limitations and capacities of PSBs compare with Mobile Money Operators (MMOs), Micro-Finance Banks (MFBs) and Super Agents.

The state of the market

Most of the earlier-mentioned benefits take into account MTN’s strengths in distribution and experience with executing similar strategies in other countries. MTN’s financial services offerings – and mobile money in general – have seen great success in places where there was no existing or sufficient banking infrastructure for providing digital financial services. In many of these mobile money-dominant countries, mobile money was the first reliable, relatively affordable and widely available financial network.

In 2006 in Kenya, only 14-19% of adults had a bank account, and only 26.7% of the entire population had access to formal financial services. The central payments switch was also just developing, and the number of bank branches were not enough to cater to citizens. Most money movements which were largely domestic remittances were through cash mules, and these were not very safe. So when M-PESA launched in 2007, it was both the first mobile money transfer service, and the safest and cheapest alternative available for the entire population.

These conditions, among other things, propelled the mobile money service to the current level of adoption. By 2019, the percentage of adults with access to formal financial services was almost 83%, a trend similar in other MTN markets such as Ghana and Uganda.

Sell more online

Paystack has all the payment tools you need to start and scale your business.

Create your free accountNigeria, however, is different from other countries that have a strong MTN mobile money presence, and a lot has also changed since the CBN first published its first mobile money regulations in 2012. Banking in Nigeria is more advanced and relatively ubiquitous than in many African countries. Many Nigerians, especially in urban areas with the highest levels of transaction activity, have and frequently use bank accounts.

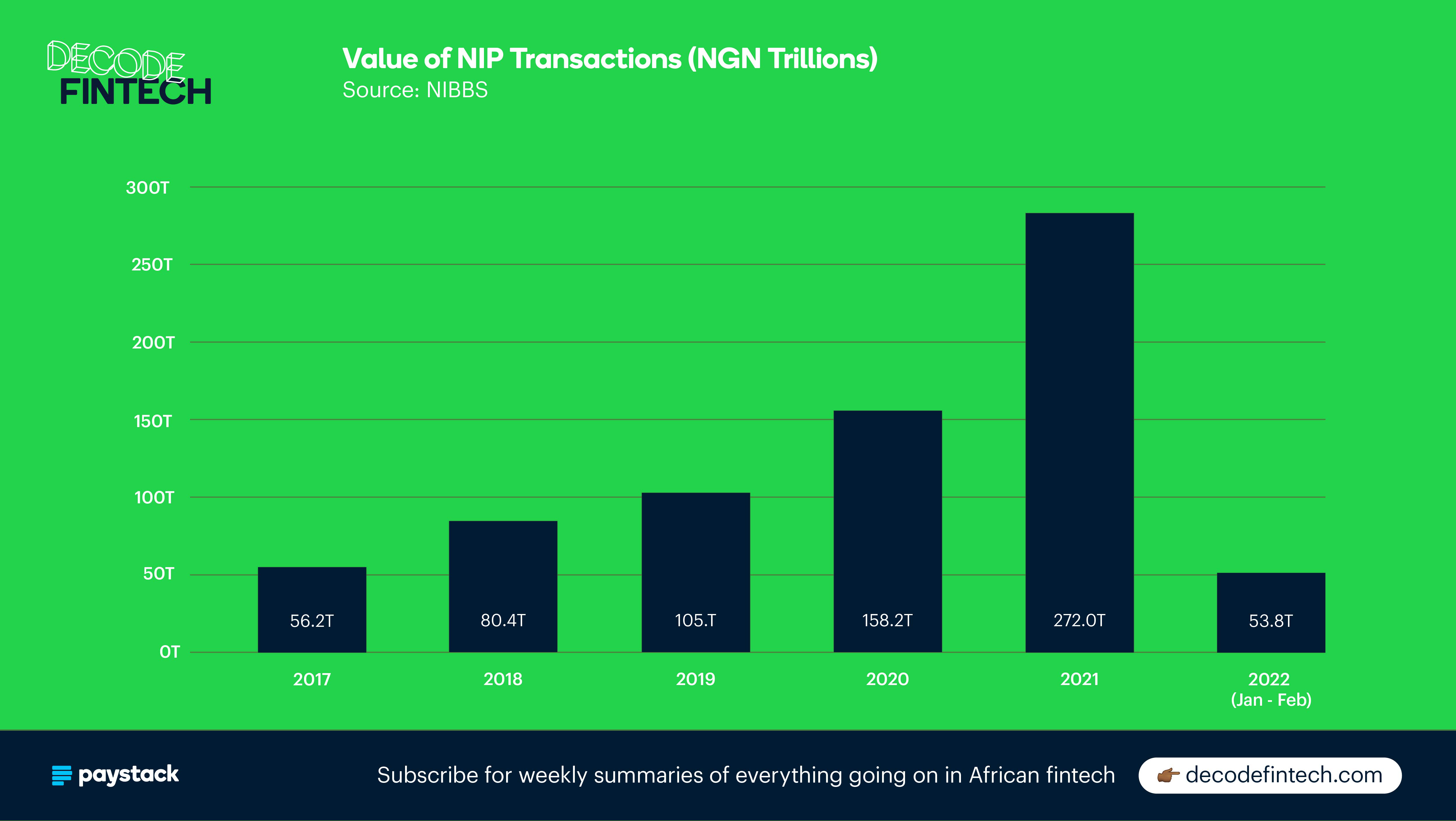

Investment in IT infrastructure and NIP, the central payments service managed by the Nigerian Inter-Bank Settlements Scheme (NIBSS) has made it super fast, easy, and cheap to do interbank transfers through a mobile phone without stepping into a bank branch.

NIP has been critical to the rise of digital payments in Nigeria. In 2021, The value of NIP transfers was ₦271 trillion (~ $650 billion), a 72% increase from 2020, and more than the total amount processed from 2017 to 2019 combined (₦224 trillion). In the first two months of 2022 alone, NIP has processed 704 million transactions worth ₦53 trillion (~$127 billion), 51% of the total amount processed in 2019 and 96% of the total amount processed in 2017.

In April 2022, Paystack Transfers, which leverages several processors including NIP had a 99.6% transfer success rate and processed 96% of these transfers in less than five minutes. This combination of speed, cost, and reliability of person-to-person transfer infrastructure has propelled trust and adoption.

In a nutshell, the Nigerian digital economy is increasingly moving at the speed of NIP.

NIP commoditises digital money movement and levels the playing field for all operators. MTN’s MoMo PSB will have to rely on more than just person-to-person transfers to differentiate itself in the market, especially for already banked users.

Beyond person-to-person transfers, commercial banks also dominate other segments of offline and digital banking. According to EfInA 2020 agent banking survey, First Bank’s First Monie was the leading agency banking provider with 37% of all active agents in the country. Other bank players like Access Bank, Zenith Bank, and GTB were not far behind.

The banks have also invested considerably in expanding their digital reach through mobile banking apps and USSD (usually in a delicate partnership with telcos). Today, millions of Nigerian customers and businesses are able to make payments, obtain cards, and apply for credit from their banks through these digital channels.

In addition, non-bank financial institutions are also competing to provide financial services to Nigerians, and the investments have followed: in 2021, the fintech industry received $1.3B in Venture Capital (VC) funding, about 72% of total VC funding for the entire year. Players like OPay, Chipper Cash and Kuda Bank have in turn aggressively invested in marketing and subsidies to rapidly drive growth. This aggressive growth expands to offline services as well: in 2021, OPay had the second most registered agents, and non-banks made up 50% of the top 10 agency banking providers, according to the EfInA agent banking survey.

The services provided by these disrupting fintechs vary widely, including some services that payment service banks are not allowed to offer: payments, savings, lending, insurance, remittance, investments, micro-pensions, and more. Beyond the breadth of services, users are also being targeted from different layers of distribution. Transsion Holdings is Nigeria’s largest provider of smart and feature phones, and is offering financial services to its base of customers through PalmPay, PalmCredit, and now InfinixWallet and TecnoWallet.

MTN should also expect competition from other telcos as well. Airtel, which launched SmartCash PSB on the same day as MTN’s MoMo’s PSB, also has a sizable base of customers and experience with mobile money in its other African and Asian markets.

Despite very strong advantages, MTN should expect a very different financial landscape compared to its other African markets.

What does this mean for fintechs?

In the weeks before MTN commenced operations of MoMo PSB, there were mixed reactions across the financial ecosystem. Some fintech industry experts speculated that MTN will “crush competition from banks and fintechs” while others had tempered or unclear expectations. In reality, this new MoMo PSB entity will likely offer an interesting balance of opportunity for both competition and collaboration in the Nigerian financial industry.

Unavoidably, MTN will attempt to drive aggressive competition. By offering customers an alternative store of value, MTN is looking to capture a sizable portion of existing payment revenues from fintechs. It’ll capture future growth by competing for unbanked users. Combining this with a near peerless distributive muscle and a deep well of resources, MTN is definitely shaping up to be a formidable provider of financial services in Nigeria.

Zooming out though, this might eventually be a net positive for both consumers and competing operators. The overall value of any network increases if more nodes of interaction are added to the network. MTN’s strategy will likely target both already banked users but also the 49.5% of Nigerians that are financially excluded or informally served.

Successfully activating financially excluded users automatically increases the number of people that can transact in the NIP-enabled interoperable payments network. This will result in not just increased revenues for MTN but for other interconnected financial institutions.

For the consumers, increased competition is likely to result in cheaper and better services as MTN and other fintechs will invest heavily in differentiating themselves in the market through better customer experience and a breadth of services.

Beyond just indirect value accretion to the overall ecosystem, there are more direct opportunities for cooperation. We have already established the limitations of the payment service bank license in providing critical financial services like lending and insurance, which are only formally available to less than 10% of the Nigerian population. Many fintechs have the regulatory approval, technical experience, and some level of distribution in providing these services to consumers and businesses. MTN can partner with these financial institutions to navigate the limitations of the payment service bank license, and unlock more opportunities to grow, by providing the following services.

Lending

MoMo PSB could work with banks and other credit providers to offer lending services to their customers. This will likely be through revenue-share agreements where the banks offer the loans to MoMo PSB customers in exchange for a fee or percentage of interest repayments. This allows MTN to increase potential average revenue per user through a higher-margin product like lending while opening partners up to a new customer base. MTN Mobile Money already has this type of lending partnership with banks in other mobile money markets, amounting to a $1.1bn loan book value by the end of 2021.

Insurance

MTN could partner with insurance companies to offer insurance products to consumers and businesses, who will make premium payments to insurance providers from their MoMo wallets. MTN has seen similar success partnering with leading Insurance providers like Sanlam in other markets. aYo, MTN’s flagship insurance product, registered 16.1m customers in 2021.

Get more stories like this

Subscribe to Decode Fintech for weekly summaries of what's going on in African fintech.

SubscribeMerchant Payments

Becoming a store of value means that MoMo PSB can facilitate money inflows and outflows from customers’ wallets. For merchant collections, MTN can integrate with PSPs like Paystack to become a payment option on the checkout. This is already possible for merchants and their customers in Ghana who use Paystack. MoMo PSB can also act as a destination for disbursements and merchant settlements and also offer niche services like dedicated virtual accounts for customer payments.

While MTN actually already offers this service directly to merchants through a set of unified mobile money APIs, partnering with other PSPs like Paystack which processes more than 50% of all online transactions in Nigeria, allows it to take advantage of the existing base of merchants to ramp up adoption.

On-ramps and alternative deposit options

To attract deposits from other bank accounts and wallets, MTN will have to ensure customers have seamless and varied options to fund their MoMo PSB wallets.

MoMo PSB is required to connect to NIBSS to receive transfers from banks and other mobile money wallets but there are other popular payment methods like cards and QR payments that MTN will likely need to partner with other payment providers for.

Card Issuing

While the PSB license does allow MTN issue debit and prepaid cards, setting up that product from scratch can be complex and time-consuming. To accelerate time to market MTN can partner with banks, card networks, and issuing startups to easily and quickly offer virtual and physical debit and prepaid cards to its customers. Debit and prepaid cards allows MTN to offer MoMo PSB customers increased options to spend money while also earning revenue from these transactions.

Remittances

MTN announced plans in their press release to offer remittance services to customers. But as explained earlier, there are regulatory restrictions on both inbound and outbound remittances. MTN can explore partnerships with banks and other licensed money transfer operators to facilitate remittances for MTN customers.

Data and Identity

Subscribers on MTN and other mobile network operators in Nigeria are being mandated by the Federal Government to link their National Identification Numbers (NIN) to their phone numbers. This is one of the biggest government-driven identification initiatives since the SIM registration exercise that started a few years ago. And while both exercises have had some challenges and affected new subscriber signups, it has allowed telcos like MTN to obtain and consolidate customer identity data that can be very valuable to other service providers in the fintech industry. MTN already offers a similar identity service in countries like Zambia but with the MoMo PSB already launched, identity solutions could potentially be explored as well.

This is a non-exhaustive list and the potential for strategic alliances expand beyond even fintech to other areas like supporting ecommerce fulfilment through agent networks and enabling government payments for agricultural subsidies and social schemes.

MTN is not new to these kinds of partnerships and has worked with different providers both in Nigeria and other African markets to notable success. According to MTN Group’s CEO Ralph Mupita in a recent earnings call, the telco will be looking to “secure strategic partnerships to support the acceleration of the group fintechs.” Some of these proposed collaborations will require special approvals from regulators and considerations for customer data and risk exposures. If successful, MTN can resolve regulatory bottlenecks and expand revenue beyond the expected PSB model.

Money, everywhere you go

The PSB license unlocks many opportunities for MTN and allows it to provide financial services to consumers at a scale that it has never done in Nigeria. It does however come with significant regulatory and revenue limitations that will require investments and strategic partnerships to overcome. MTN will be looking to employ capital, expertise, partnerships, and sheer distribution to turn the color of money in Africa’s most populous country into yellow and black.

With competition from banks, fintechs and other telcos, it’s too early to predict definite success but all signs indicate an incoming shift in the financial services landscape.

We hope this article has provided an illuminating lens into the different ways in which MTN might leverage this license to provide financial services. To get more news and analysis about how fintech is evolving in Africa subscribe to the Decode Fintech Newsletter.